If you are between age preservation age and 65, putting in place a transition to retirement strategy could allow you to:

Transition to Retirement

- ease into retirement by reducing working hours without reducing your net income

- boost your retirement savings without impacting your net income if you are still working full time

For those nearing the retirement years, you can enjoy a better lifestyle now and a greater super balance at retirement.

Until recently, you could only access your super once you turned 65 or retired. This meant it was difficult to reduce your work hours and still maintain your standard of living. With the new rules, you can withdraw some or your entire super over into a retirement income stream. Then you can top up your reduced income by drawing on your super.

However, you must be aware of the impact this can have on you and your circumstances. Some parts of this measure are complex to understand, set up and maintain, so your financial adviser can help you decide if this option is right for you.

Accessing your super benefits

Under the transition to retirement rules you can only access your super benefits as a ‘non-commutable’ income stream. This generally means you cannot take your benefits as a lump sum cash payment while you are still working. You must take your super benefits as regular payments.

We recommend you:

- check if your superannuation fund offers non-commutable income streams

- seek financial advice to find out what is best for you.

Funds offering income streams

It is not compulsory for super funds to offer you a non-commutable income stream.

If your superannuation fund doesn’t offer an income stream which lets you take up the transition to retirement option, you may be able to choose a new super fund.

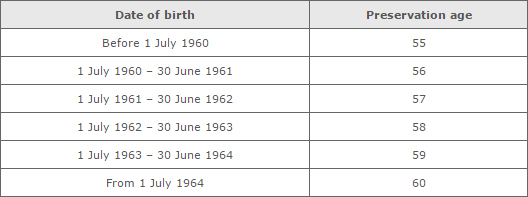

Understanding preservation age

Your preservation age is generally the age you are allowed to access your super benefits when you stop working.

The table below shows your preservation age. Once you reach your preservation age, you can access your super benefits without retiring completely from the workforce.

Table: Your preservation age depends on your date of birth

Tax on transition to retirement income streams

Transition to retirement income streams are taxed in the same way as other income streams.

That means:

- if you’ve reached your preservation age and are less than 60 years old, the taxable part of your income stream will be taxed at your marginal tax rate. If your income stream is paid from a taxed source, you will also receive a tax offset equal to 15% of the taxable part of the income stream, and

- once you turn 60, your super income from a taxed source will be tax-free.

Transition to retirement

Once you reach your preservation age, you can access your super before you retire but only in the form of a ‘non-commutable’ income stream, not a lump sum.

This means, if you are preservation age or over, you can reduce your working hours without leaving your job or reducing your total income. You can top-up your income with a regular income stream from your super savings.

Limits on the transition to retirement measure

Under the transition to retirement measure you are required to take no more than 10% of the account balance, as a pension payment(s) in each financial .

Members should discuss this issue with their superannuation fund as funds will have their own rules.

Super guarantee contributions

Employers still need to make compulsory super guarantee contributions for all their eligible employees.

Contact Information

Phone: 08 8373 7277

Fax: 08 8357 0366

Email: admin@pgfs.com.au

Facebook: PGFS

Quicklinks