Payment of Benefits

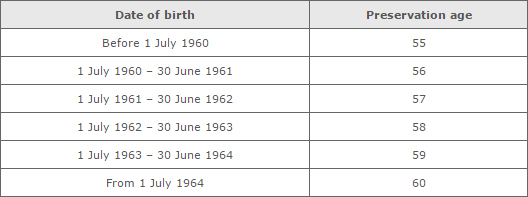

Generally, you must reach your preservation age before you can access your super. Use the following table to work out your preservation age.

Preservation age is not the same as pension age. Pension age is when you become eligible for government pension benefits, depending on your income and assets.

There are three super benefit categories:

- preserved

- restricted non-preserved

- unrestricted non-preserved.

There are rules for how you can access each category. There is no requirement for the fund to pay these benefits once a member reaches a certain age. Benefits need to be cashed as soon as practicable after a member dies.

Preserved benefits

Generally, you cannot access preserved benefits from a super fund or retirement savings account until you have satisfied a condition of release.

Restricted non-preserved

As long as your employer or your employer’s associates have made superannuation contributions on your behalf, your fund can pay you restricted non-preserved benefits if that employment is terminated. They can also pay you under the same conditions as preserved benefits.

Unrestricted non-preserved

These are benefits you voluntarily kept within the super system after you met a condition of release. If the super fund rules allow the payment, your fund can pay you these benefits at any time on demand, regardless of your:

- age

- employment situation

- financial position.

Conditions of release

You must meet a condition of release before your super fund can pay you a benefit. Your fund can only pay benefits if the fund’s rules allow it.

Your fund can pay your benefits under the following conditions of release, provided the fund’s rules allow it:

- retirement

- transition to retirement

- attaining age 65 or more

- your benefits are less than $200

- terminating gainful employment

- terminal medical condition

- permanent incapacity

- temporary incapacity

- compassionate grounds

- severe financial hardship

- release of benefits under an ATO release authority.

There may be restrictions as to how the benefit may be paid.

Accessing your super before you retire

You can only access lump sum super benefits before your preservation age in very limited circumstances. For example, if you:

- need to meet expenses associated with a medical condition or other compassionate grounds

- are experiencing severe financial hardship

- are a temporary resident departing Australia

- have a terminal medical condition.

Compassionate grounds

You must send your application to the Australian Prudential Regulation Authority (APRA) if you want to access your super benefits early due to compassionate grounds.

Terminal medical condition

If you have a terminal medical condition, you can apply to your super fund to access your super benefits tax-free, regardless of your age.

The final decision to release your super benefits is subject to the rules of the fund.

Transition to retirement

Once you reach your preservation age, you can access your super before you retire but only in the form of a ‘non-commutable’ income stream, not a lump sum.

This means, if you are 55 years old or over, you can reduce your working hours without leaving your job or reducing your total income. You can top-up your income with a regular income stream from your super savings.

Contact Information

Phone: 08 8373 7277

Fax: 08 8357 0366

Email: admin@pgfs.com.au

Facebook: PGFS

Quicklinks