Establishing a self managed (“do it yourself”) superannuation fund is becoming increasingly commonplace in Australia and is the alternative option to using an independently managed super fund (such as available through employer, retail or industry based superannuation providers).

Self managed super funds perform the same function as other super funds, namely to provide retirement and other ancillary benefits for their members. The key difference, however, is that members of self managed funds must also act as trustees and are therefore ultimately responsible for all investment decisions and the ongoing management of their fund.

Why establish a self managed super fund?

People may decide to establish a self managed super fund for reasons such as:

1) Control – trustees have complete control over the fund and its investments (within the legislative framework). This is attractive to those who wish to be more involved in the management of their monies.

2) Flexibility in investment decisions – trustees are able to invest in any approved assets, which may include investments such as shares, property (including direct residential or commercial) or managed funds. More advanced strategies such as investing in business real property, using gearing or borrowing (in certain circumstances) or active direct share investing, are possible, which can provide additional scope to maximize ones retirement assets. These avenues are generally unavailable through traditional superannuation channels.

3) Estate planning – Future generations may be more effectively cared for, through the greater flexibility provided via a SMSF. In addition, SMSF’s can be tailored to meet your specific estate planning needs, compared to other alternatives which have to meet the needs of many investors.

4) Cost Effectiveness – For larger amounts, SMSF’s may be particularly cost effective, as many costs are fixed and therefore fall as a percentage, as the amount of invested funds increases.

5) Tax Advantages – Whilst self managed super funds operate under same taxation rules as any other super fund, they may allow a more transparent and effective approach to minimizing tax payable. For example, funds may be managed to specifically provide tax advantages beyond those generally available to members. These may include investing to maximizing imputation credits via Australian equities or depreciation via direct property, which can reduce tax payable (including contributions tax).

6) Holistic Approach – SMSF’s have the ability to provide for one or more members (often family members) wealth accumulation and pension needs. This means they may be used in a holistic manner throughout a members lifetime.

As a SMSF trustee, you are ultimately responsible for running your SMSF. It is important you understand the duties, responsibilities and obligations of being a trustee. These responsibilities may include:

Some of the key restrictions under the SIS Act include:

Significant penalties may apply for trustees not meeting their obligations.

Who is a SMSF suitable for?

While SMSFs are great for some people, they don’t suit everyone. Managing your own super takes time, knowledge, skill and money, so before deciding to set up a SMSF, it’s important to consider these issues. Should you wish to take advantage of a SMSF to assist in your retirement planning, but don’t have the ability or willingness to perform the various administration or investment functions, utilising an advisory service can assist in this regard.

If you don’t already have your own DIY super fund but are interested in setting one up, an adviser at PGFS can assist in this process, its administration over time and the management of the funds assets. Alternatively, if you have a SMSF and wish to consider your options to improve its performance or management, please call us or e-mail info@pgfs.com.au.

If you are between age 55 – 75, putting in place a transition to retirement strategy could save you thousands by allowing you to:

For those nearing the retirement years, you can enjoy a better lifestyle now and a greater super balance at retirement.

Until recently, you could only access your super once you turned 65 or retired. This meant it was difficult to reduce your work hours and still maintain your standard of living. With the new rules, you can withdraw some or your entire super over into a retirement income stream. Then you can top up your reduced income by drawing on your super.

However, you must be aware of the impact this can have on you and your circumstances. Some parts of this measure are complex to understand, set up and maintain, so your financial adviser can help you decide if this option is right for you.

Accessing your super benefits

Under the transition to retirement rules you can only access your super benefits as a ‘non-commutable’ income stream. This generally means you cannot take your benefits as a lump sum cash payment while you are still working. You must take your super benefits as regular payments.

We recommend you:

Funds offering income streams

It is not compulsory for super funds to offer you a non-commutable income stream.

If your superannuation fund doesn’t offer an income stream which lets you take up the transition to retirement option, you may be able to choose a new super fund.

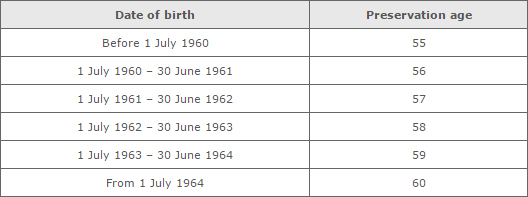

Understanding preservation age

Your preservation age is generally the age you are allowed to access your super benefits when you stop working.

The table below shows your preservation age. Once you reach your preservation age, you can access your super benefits without retiring completely from the workforce.

Table: Your preservation age depends on your date of birth

Tax on transition to retirement income streams

Transition to retirement income streams are taxed in the same way as other income streams.

That means:

Limits on the transition to retirement measure

There is no specific limit on the amount of superannuation benefits that may be drawn down under the transition to retirement measure other than the requirement that no more than 10% of the account balance, as at the start of the financial year, may be paid each year.

Members should discuss this issue with their superannuation fund as funds will have their own rules.

Super guarantee contributions

Employers still need to make compulsory super guarantee contributions for all their eligible employees.

Salary Sacrifice Contributions

If you make super contributions under an effective salary sacrifice arrangement, you may be able to increase your superannuation balance by reducing your assessable income for taxation purposes.

Super contributions are not a fringe benefit.

If salary sacrificed super contributions are made to a complying super fund, the sacrificed amount is not considered a fringe benefit for tax purposes.

Your employer will not:

Salary sacrificed contributions are treated as employer contributions. If salary sacrificed super contributions are made to a non-complying super fund, the contributions will be a fringe benefit.

Your employer will:

Super contributions are deductible for your employer

If you are under 75 years old, your employer can usually claim a tax deduction on the amount of salary sacrificed contributions they contribute to your super fund on your behalf.

Salary sacrifice reduces your assessable income

The sacrificed component of your total salary package is not your assessable income for taxation purposes. This means that it is not subject to pay as you go (PAYG) withholding tax.

Salary sacrifice is a reportable employer super contribution

As you influence the amount of the extra super contributions your employer makes to your super fund, any salary sacrificed amounts will be reportable employer superannuation contributions. The reportable employer super contribution will be included on your payment summary and will affect the income tests for some tax offsets and deductions, the Medicare levy surcharge, and certain government benefits and obligations.

Super contributions are concessionally taxed in the fund

If you make super contributions through a salary sacrifice agreement, these contributions are taxed in the super fund at a maximum rate of 15%.

Generally, this amount of tax is less than what you would pay if you did not enter into a salary sacrifice agreement and instead were subject to PAYG withholding tax on your earnings.

However, the concessional tax treatment is limited to a set amount of contributions made each income year.

On 1 July 2016, Sally and Zoe started work at Green Thumb Gardening, earning $45,000 a year. Zoe entered into a salary sacrifice arrangement with her employer to sacrifice $10,000 of her earnings into her super fund. Sally did not salary sacrifice any of her salary.

The following table shows the difference between Sally and Zoe’s assessable income and rates of tax at the end of the 2016–17 income year:

Superannuation rates and thresholds

The following is brief overview of the current key rates and thresholds that apply in relation to superannuation.

New Government supperannuation support for low income earners

Reduction of the Governemtn co-contribution

Coinciding with the commencement of LISC from july 1 2012, the Government co-contribution (relevant to non-concessional contributions) is expected to decrease.

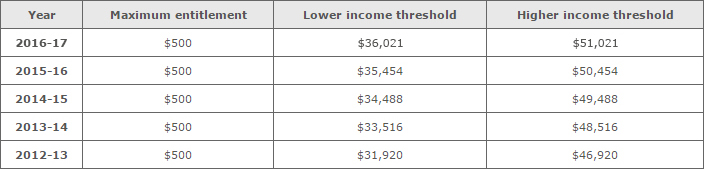

Co-contribution income thresholds

The lower income threshold is indexed in line with AWOTE each income year. However, government proposals have led to the lower limit threshold being frozen for the 2010-11 and 2011-12 years.

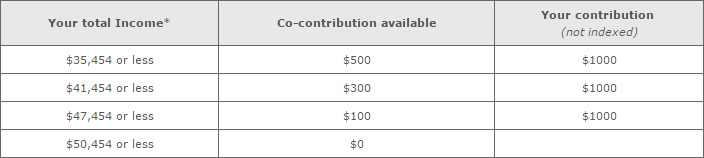

Example benefit for contributions

How much you’ll receive depends on you income. For every dollar you contribute from your after-tax income, the Government will put in 50 cents, up to a maximum of $500. Use our contributions advisor calculator or the table below.

Superannuation guarantee (SG)

The superannuation guarantee requires employers to contribute a minimum of 9.5% of an eligible employee’s earnings (ordinary time earnings) to a complying super fund or retirement savings account (RSA). Your contributions need to be made at least every quarter.

Maximum super contribution base

* Indexed in line with AWOTE each income year.

Concessional contributions cap (CCC)

Concessional contributions include:

Concessional contributions cap for people 49 years old or over

The concessional contribution cap

The temporary higher contributions include personal contributions for which you do not claim an income tax deduction.

Non-concessional contributions cap (NCCC)

Non-concessional contributions include:

Small business exclusion (CGT cap)

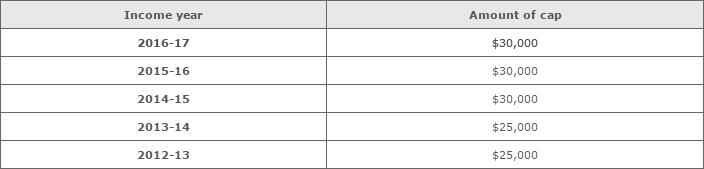

* The untaxed plan cap amount is indexed in line with AWOTE, in increments of $5,000 (rounded).

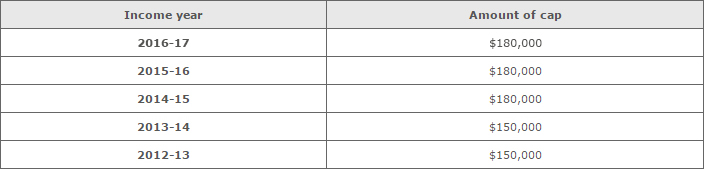

* The application of the low rate threshold for super lump sum payments is capped at $195,000 (2016/17).

^ The untaxed plan cap is $1,415,000 (2016/17).

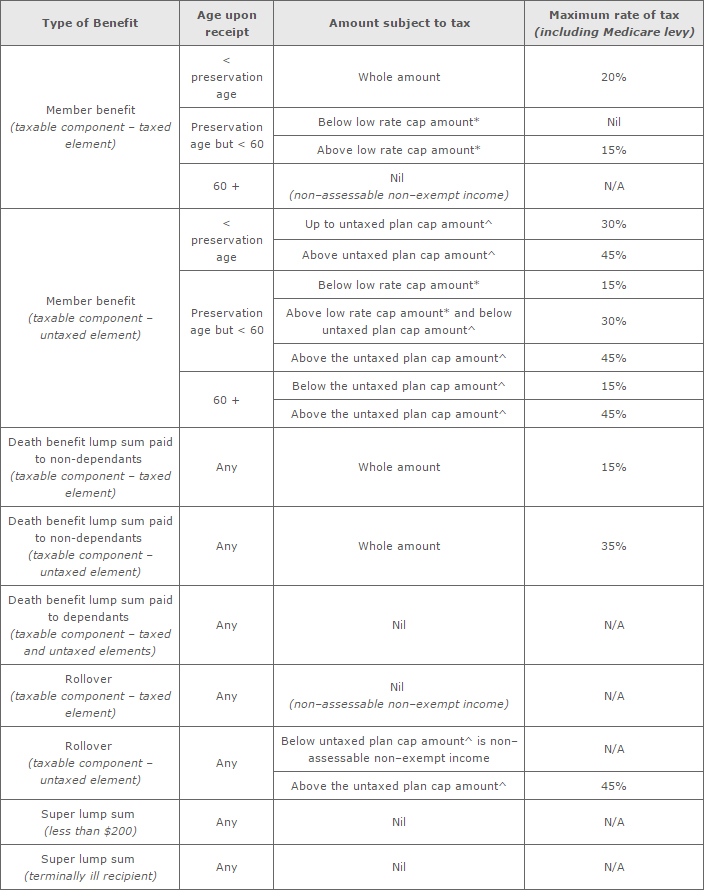

Payment levels from income streams (super)

Super income stream tax tables

The tax-free component of any income drawn is not assessable and not exempt income in all cases.

Medicare levy (2%) will apply if amounts are assessable.

The tax-free component of any income drawn is not assessable and not exempt income in all cases.

Medicare levy (2%) will apply if amounts are assessable.

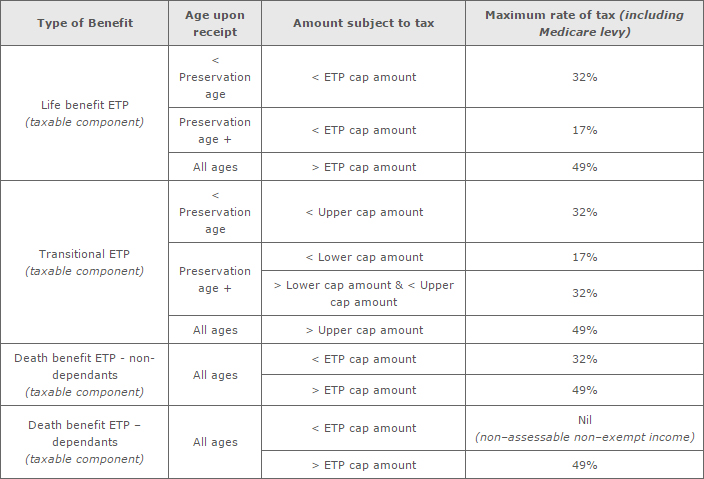

Employment termination payments

An employment termination payment (ETP) is a payment made in consequence of the termination of employment. It can include:

ETP cap amount for termination payments:

* The ETP cap amount is indexed in line with AWOTE, in increments of $5,000 (rounded).

Transitional ETP cap amounts up to 30 June 2016

Transitional arrangements apply if you were entitled, as at 9 May 2006, to a payment made on the termination of employment under:

Employment termination payments made after 1 July 2007 (other than those made under the transitional arrangements) won’t be able to be contributed to or rolled over into super.

The taxable component of a transitional termination payment will be taxed at:

Superannuation been specifically designed and endorsed by the Federal Government as a preferred way to save for your retirement, and has, therefore, unique tax benefits that make it particularly attractive.

Superannuation can be a tax effective way of building wealth for your retirement. The tax rates imposed will differ depending on what stage of life you are at and in what manner the super funds invested are held.

Accumulation v Income Stream (Pension phase)

There are 2 primary methods of holding your super investments:

These superannuation tax rates are in contrast to personal marginal tax rates, which could be considerably higher.

When can I access my benefits?

Generally, you must reach your preservation age before you can access your super. Use the following table to work out your preservation age.

Preservation age is not the same as pension age. Pension age is when you become eligible for government pension benefits, depending on your income and assets.

There are three super benefit categories:

There are rules for how you can access each category. There is no requirement for the fund to pay these benefits once a member reaches a certain age. Benefits need to be cashed as soon as practicable after a member dies.

Generally, you cannot access preserved benefits from a super fund or retirement savings account until you have satisfied a condition of release.

As long as your employer or your employer’s associates have made superannuation contributions on your behalf, your fund can pay you restricted non-preserved benefits if that employment is terminated. They can also pay you under the same conditions as preserved benefits.

Unrestricted non-preserved

These are benefits you voluntarily kept within the super system after you met a condition of release. If the super fund rules allow the payment, your fund can pay you these benefits at any time on demand, regardless of your:

You must meet a condition of release before your super fund can pay you a benefit. Your fund can only pay benefits if the fund’s rules allow it.

Your fund can pay your benefits under the following conditions of release, provided the fund’s rules allow it:

There may be restrictions as to how the benefit may be paid.

Accessing your super before you retire

You can only access lump sum super benefits before your preservation age in very limited circumstances. For example, if you:

Terminal medical condition

If you have a terminal medical condition, you can apply to your super fund to access your super benefits tax-free, regardless of your age.

The final decision to release your super benefits is subject to the rules of the fund.

Once you reach your preservation age, you can access your super before you retire but only in the form of a ‘non-commutable’ income stream, not a lump sum.

This means, if you are 55 years old or over, you can reduce your working hours without leaving your job or reducing your total income. You can top-up your income with a regular income stream from your super savings.